Mobile Gaming’s Quiet Comeback in Revenue and Monetization

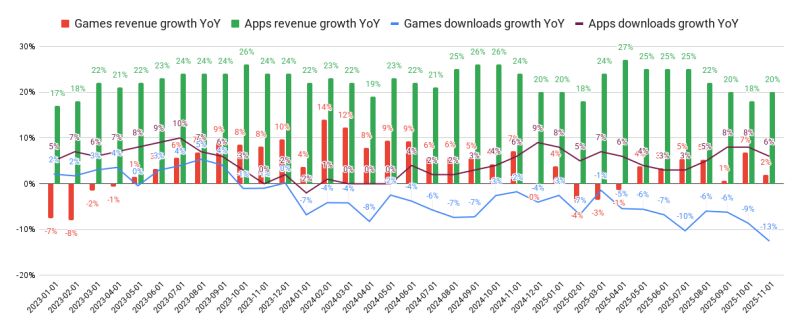

Looking at the growth of Mobile Games & Apps over the past few months, we see a healthy upward trend in revenue and monetization (based on Sensor Tower data, including Android and iOS, excluding China).

While growth is more pronounced in non-gaming Apps, the mobile gaming sector has improved compared to 2024 and early 2025. Furthermore, since this data excludes in-game advertising, in-app advertisign and Direct-to-Consumer (DTC) payments, the actual market growth is likely even stronger.

However, a concerning trend has emerged—particularly in gaming, but increasingly in apps: downloads are outpacing revenue growth. In several markets, the gap between download volume and monetization is widening.

Key hypotheses for this gap:

🔹 Market Saturation: A massive volume of existing content and longer app lifecycles mean new entries must compete with established giants.

🔹 Rising quality standards: the “bar” for quality is higher than ever, making it harder to stand out.

🔹 Risk aversion: The industry has become more conservative, focusing on iterations of existing concepts rather than innovation (it is easier to get investment for such content unless you have strong network that can back you up). This leads to lower user motivation to try “new” content that feels really different than what people saw already..

🔹 Focus on decreasing the risk in Growth: A heavy focus on early monetization (e.g., tROAS bidding) minimizes risk but forces advertisers to compete for the same narrow pool of high-value users repeatedly…

How do you see it? Any comments?